Note that [latex]P/Y[/latex] and [latex]C/Y[/latex] are not main button keys in the [latex]TVM[/latex] row. The P/Y and C/Y variables are located in the secondary function accessed by pressing 2nd I/Y. The calculator has a large LCD screen at the top which is displaying the number “0.”.

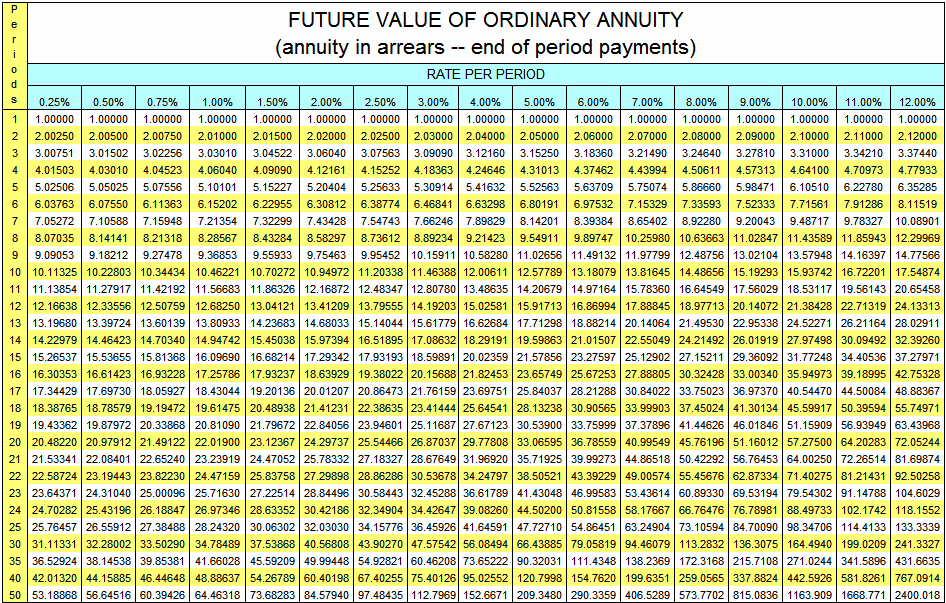

\boxed2.2[/latex] Future Value of Ordinary Annuities

Continuing with our example, if I agreed to make the $100 annual payments at the beginning of each year, our arrangement would be considered to be an annuity due. That depends on the agreed upon interest rate and on whether or not we agreed to an ordinary annuity or to an annuity due. From your perspective, the periodic amounts represent deposits, as in, you can deposit the amounts into an interest earning account as you receive them. Note that if you are not sure what future value is, or you wish to calculate future value for a lump sum, please visit the Future Value of Lump Sum Calculator. That’s because $10,000 today is worth more than $10,000 received over the course of time. Once the contribution (accumulation) phase is completed, they will receive a fixed rate of return on these contributions.

Fixed Annuity Calculator

In this context, an “ordinary annuity” is the same as an immediate fixed annuity, meaning that the holder of the annuity will begin to immediately receive payments for the rest of their life. The formula above is for an “ordinary annuity,” which is an annuity that involves making payments at the end of each payment period. This makes quite a bit of difference in an annuity’s perceived value, due to the time value of money. These annuities involve making a large lump sum payment and immediately gaining access to an annual payout for the rest of your life. These annuities will give you an income right away, although they require a larger initial payment and might not keep pace with inflation.

Total Payments

Therefore, this compensation may impact how, where and in what order products appear within listing categories, except where prohibited by law for our mortgage, home equity and other home lending products. Other factors, such as our own proprietary website rules and whether a product is offered in your area or at your self-selected credit score range, can also impact how and where products appear on this site. While we strive to provide a wide range of offers, Bankrate does not include information about every financial or credit product or service. Click here to sign up for our newsletter to learn more about financial literacy, investing and important consumer financial news.

With just a few data points, you can decide if an annuity will provide the investment return that meets your financial needs. Annuities are special investments issued by insurance companies that are designed to provide a stable, consistent payment to the investor. In most cases, the insurance company guarantees a certain payment regardless of the condition of the market. This is useful for retired people since the payments will continue for the policyholder’s life.

- An annuity is a financial contract that offers a stream of income, often in retirement, in exchange for money paid into the annuity.

- It is important to note that variable annuities do not guarantee the return of principal.

- A fluctuating interest rate environment can significantly alter the future value of annuities, necessitating periodic re-evaluation of financial plans.

- Unless insurance companies go bankrupt, fixed annuities promise the return of principal.

Interest rate(i):

In addition to calculating the present and future values, you will also have the ability to calculate the value of the annuity payout. This formula is logarithmic, which is why an annuity payment calculator can be helpful. Annuities can be a valuable financial asset for retirement planning and establishing future sources of cash flow.

Laura started her career in Finance a decade ago and provides strategic financial management consulting. This calculator helps individuals determine their net worth by subtracting their liabilities from their assets, giving a snapshot of their financial health. The best way to demonstrate the strengths of the annuity calculator is to take some annuity examples. When you set all the required parameters, you will immediately see the results summarized in a table. You can also follow the progress of your annuity balance in a dynamic chart and annuity table of the payment schedule. In general, types of annuities are classified according to the following features.

It’s useful for understanding how much a sum of money now will be worth in the future, considering the average inflation rate. In essence, the future value of the annuity is a powerful tool that provides a clear and quantifiable understanding of the long-term implications of financial choices made today. Whether for personal savings, investment planning, or retirement preparations, mastering this concept is key to building a secure and predictable financial what is an invoice what is it used for future. Investment Management Fees–Similar to management fees paid to portfolio managers of mutual funds and ETFs, variable annuity investments also require fees to pay portfolio managers. Most people use annuities as supplemental investments in combination with other investments such as IRAs, 401(k)s, or other pension plans. Many people find that as they get older, investment options with tax shields approach or reach their contribution limits.

An annuity due, by contrast, is a series of recurring payments that are made at the beginning of a period. In contrast to the FV calculation, PV calculation tells you how much money would be required now to produce a series of payments in the future, again assuming a set interest rate. An annuity is defined as a series of equal cash amounts (cash flows, payments, deposits, etc).